The landscape of global finance is currently undergoing a profound transformation as central banks strive to integrate decentralized technology into the bedrock of national economies without compromising safety. In a major step toward this goal, the Bank of England recently finalized its draft Code of Practice for systemic stablecoin issuers, aiming to create a robust regulatory framework that mirrors the security of traditional sterling. This initiative is designed to ensure that digital assets functioning as money are backed by high-quality reserves and remain fully redeemable at par, providing consumers with the same confidence they have in commercial bank deposits. By establishing clear rules of the road, the United Kingdom is positioning itself as a leader in the next generation of financial infrastructure, allowing for the growth of programmable payments and more efficient cross-border settlement. The focus remains on resilience, ensuring that even as new technologies emerge, the underlying stability of the British pound remains completely unquestioned and protected from market volatility.

Strategic Adjustments to Asset Management and User Limits

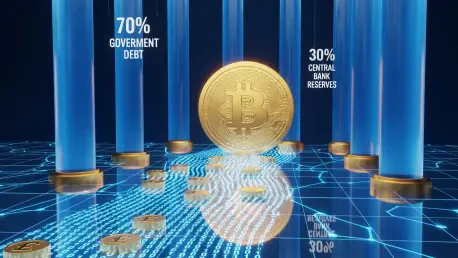

Refined Rules: Balancing Reserves and Issuance Caps

The updated regulatory framework introduces a more flexible approach to asset backing, acknowledging the need for stablecoin issuers to maintain viable business models while operating under central bank scrutiny. While early proposals leaned toward a strict requirement for one hundred percent central bank deposits, the new guidelines permit firms to hold up to seventy percent of their backing assets in short-term government debt, such as UK Gilts. This shift allows for a sustainable revenue stream while ensuring that the assets remain highly liquid and easily convertible during periods of high redemption pressure or market stress.

Such a balance is critical for the long-term health of the digital asset ecosystem, as it prevents the strangulation of innovation by overly restrictive capital requirements. By allowing a significant portion of reserves to be held in interest-bearing government securities, the Bank of England is encouraging competition among private issuers who can now offer more sophisticated services. However, the remaining thirty percent must still reside in central bank accounts to provide an immediate liquidity buffer, ensuring that every digital token can be exchanged for fiat currency without any delay or loss of value to the user.

Guardrails: Transitioning From Individual to Systemic Caps

One of the most significant changes in the final draft is the pivot away from restrictive individual holding limits that would have capped the amount of digital currency in personal wallets. Initially, policymakers were concerned that a rapid migration of funds from traditional savings accounts into stablecoins could destabilize the retail banking sector. To address this without hindering user convenience, the Bank has opted for a macro-level approach, implementing an aggregate forty billion pound limit for each systemic stablecoin instead of monitoring every single citizen’s transaction habits or total digital storage capacity.

This systemic guardrail provides a safety net for the broader economy by preventing any single private currency from growing so large that its failure would jeopardize national financial stability. It also allows households and businesses to utilize these digital tools more freely, fostering a more inclusive environment for retail payments and programmable money applications. By focusing on the total market capitalization rather than the individual user, the regulator maintains a high-level view of liquidity risks while allowing the market to grow organically within safe, clearly defined boundaries.

Collaborative Oversight and the Roadmap to Implementation

Unified Supervision: Dividing the Bank and FCA Mandates

Navigating the complexities of digital asset regulation requires a coordinated effort between the nation’s primary financial watchdogs to avoid regulatory arbitrage and ensure consumer safety. Under the new regime, the Bank of England will directly supervise stablecoin issuers that reach a systemic status, meaning their scale and connectivity are significant enough to impact the entire economy. Meanwhile, the Financial Conduct Authority will retain oversight of smaller issuers and those primarily used for investment or speculative trading, ensuring that every asset falls under a specific and appropriate jurisdiction.

This tiered approach provides a clear ladder of regulation for growing fintech companies, allowing them to start under the flexible guidance of the FCA before graduating to the more stringent requirements of the central bank. Close cooperation between these two entities ensures that there is no regulatory gap during this transition, protecting consumers at every stage of a company’s development. This synergy is intended to streamline compliance for firms operating in the United Kingdom, making the region an attractive destination for global innovators seeking a predictable and fair legal environment for their operations.

Strategic Horizon: Achieving Full Operational Status by 2027

The roadmap toward full implementation is marked by a series of deliberate milestones designed to give the industry ample time to adjust to these high standards. With a target for full operational status set for 2027, the Bank of England has scheduled several rounds of technical consultation to refine the intricacies of redemption rights and operational resilience. This period of engagement is crucial for identifying potential bottlenecks in the technology stack, ensuring that the final systems are capable of handling millions of transactions without compromising the security of the ledger.

Furthermore, this timeline provides a clear signal to international investors and developers that the United Kingdom is committed to a stable and forward-looking financial policy. By providing a multi-year lead time, the central bank is reducing the uncertainty that often plagues the digital asset space, encouraging long-term capital investment in local infrastructure. This structured rollout is expected to culminate in a financial ecosystem where digital sterling and traditional bank deposits coexist seamlessly, each serving different needs while operating under a unified umbrella of sovereign protection.

Looking Ahead: The Future of Sovereign Digital Payments

The transition toward a regulated stablecoin environment represented a pivotal shift in how the nation conceptualized the relationship between technology and sovereign value. By prioritizing the seventy-thirty reserve split and replacing individual caps with systemic guardrails, the Bank of England successfully created a blueprint that balanced growth with safety. This framework ultimately offered a template for other nations seeking to integrate private digital assets into their domestic economies without ceding control over monetary stability. Moving forward, the industry must focus on interoperability, ensuring that these systemic stablecoins can work across different blockchain networks and traditional payment rails. Firms should prioritize building robust compliance departments that can handle the real-time monitoring required by the central bank. As these digital tools became a standard part of the financial toolkit, the integration of programmable features redefined commercial contracts and automated settlements. The lessons learned during this regulatory phase suggested that transparency and frequent dialogue were the most effective ways to build a resilient and innovative digital future.