The recent economic forecast provided by the Organization for Economic Cooperation and Development suggests that the United Kingdom is currently navigating its most precarious financial trajectory since the global downturn of the early century, placing the nation at a higher risk of stagnation than any other G7 member. This grim assessment comes at a time when the domestic market is already reeling from a series of high-profile failures that indicate a systemic weakness in the broader economy. While government officials maintain that the current fiscal trajectory is necessary for long-term stability, the immediate reality for businesses and households is one of shrinking margins and diminishing purchasing power. The juxtaposition of rigid fiscal targets against a backdrop of declining industrial output has created a volatile environment where the margin for error has essentially disappeared. Consequently, the debate over whether the current policy framework is a safeguard or a catalyst for a deeper recession has moved to the forefront of national discourse.

Industrial Fragility and Market Signals

The Erosion of High-Street Retail and Manufacturing

The collapse of iconic high-street institutions like Russell & Bromley serves as a visible barometer for the cooling consumer environment that has gripped the British economy. Such closures are not merely isolated incidents of corporate mismanagement but rather symptoms of a retail landscape that is being suffocated by high operational costs and shifting consumer priorities. When established brands with significant heritage can no longer sustain their brick-and-mortar presence, it signals a fundamental breakdown in the traditional economic engine of the urban center. Furthermore, this trend is exacerbated by the rising costs of business rates and the general decline in disposable income among the middle class, who have historically been the primary drivers of retail growth. The resulting vacancies in commercial hubs create a feedback loop of declining foot traffic and reduced local tax revenue, further straining the ability of municipalities to support local infrastructure and services.

Manufacturing sectors are facing equally daunting challenges, as evidenced by recent production halts at major facilities like those operated by Jaguar Land Rover. These disruptions are largely attributed to persistent supply chain vulnerabilities and the rising cost of critical components, which have become increasingly difficult to source in a fragmented global trade environment. The inability to maintain consistent production schedules not only impacts domestic output but also threatens the UK’s standing as a competitive hub for advanced automotive engineering and export. As industrial giants struggle to manage these logistical hurdles, the ripple effects are felt throughout the extensive network of smaller suppliers that depend on steady production volumes for their survival. Without a significant shift in the approach to industrial strategy and trade facilitation, the manufacturing base remains highly susceptible to external shocks that could permanently diminish its contribution to the national gross domestic product.

Escalating Operational Costs and Labor Pressures

The government’s decision to implement a 4.1% increase in the living wage has introduced a complex set of challenges for employers who are already struggling to balance their books in a period of low growth. While the policy is intended to provide much-needed relief to low-income workers facing a high cost of living, it also adds a significant financial burden to the very businesses that are expected to drive job creation. For many small and medium-sized enterprises, this mandated wage hike represents a substantial increase in overhead that may force difficult decisions regarding staffing levels or service pricing. In sectors with thin profit margins, such as hospitality and social care, the added labor cost could become the deciding factor in whether a business remains viable or is forced to consolidate. The timing of this increase, occurring alongside other rising costs, creates a cumulative pressure that threatens to stifle the entrepreneurial spirit required for economic recovery.

Beyond the immediate impact on payroll, the broader labor market is also being reshaped by the interaction between inflation and wage growth, often leading to increased industrial action and demands for further compensation. As the Bank of England considers its next moves regarding interest rates, the potential for a wage-price spiral remains a significant concern for economists who are monitoring the balance between consumer demand and inflationary pressure. The persistent nature of core inflation means that even as wages rise, the real-world purchasing power of citizens remains largely stagnant, leading to a sense of frustration that permeates the workforce. This environment of economic uncertainty makes it difficult for companies to plan for long-term expansion or investment, as the cost of capital and labor remains unpredictable. Consequently, the labor market is becoming increasingly defensive, with both employers and employees prioritizing stability over the risk-taking that is typically associated with a thriving and dynamic modern economy.

Structural Policy and Fiscal Challenges

The Cost of Energy Transition and Geopolitical Risk

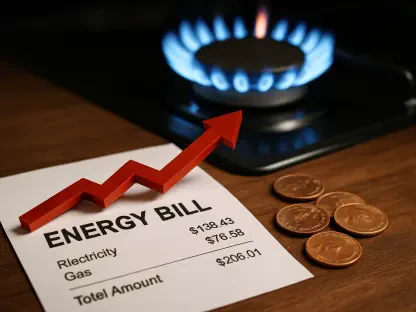

Britain’s aggressive pursuit of net-zero carbon emissions has placed the nation in a unique position where its energy policy is both a point of environmental leadership and a source of economic vulnerability. The rapid transition away from traditional energy sources has increased the country’s reliance on expensive energy imports, leaving the domestic market highly sensitive to fluctuations in global commodity prices. This vulnerability is particularly evident as geopolitical tensions in the Middle East threaten to disrupt supply routes and drive up the cost of oil and gas on the international stage. High energy costs act as a pervasive tax on every sector of the economy, from heavy industry to domestic households, further eroding the competitive advantage of British manufacturers. While the long-term benefits of green energy are frequently cited by policymakers, the short-term economic pain of high utility prices is creating a barrier to growth that is proving difficult to overcome.

The intersection of energy security and monetary policy has also become a critical focal point for the Bank of England as it attempts to manage the current inflationary environment. If energy prices continue to climb due to external conflicts or supply constraints, the central bank may find itself compelled to maintain or even increase interest rates to prevent inflation from becoming entrenched. Such a move would further increase the cost of borrowing for businesses and mortgage holders, potentially triggering a sharper contraction in consumer spending than previously anticipated. The risk of a “stagflationary” scenario—where growth remains flat while prices and interest rates rise—is a persistent threat that complicates the government’s fiscal planning. This delicate balancing act requires a level of policy flexibility that many critics argue is currently lacking in the Treasury’s rigid adherence to its established fiscal mandates and spending commitments.

Fiscal Drag and the Taxation Blizzard

One of the most contentious aspects of current fiscal policy is the phenomenon of fiscal drag, which occurs when the government freezes tax thresholds while nominal wages continue to rise. This practice effectively pulls more taxpayers into higher tax brackets, resulting in a quiet but substantial increase in the overall tax burden for millions of workers across the country. While this strategy provides the Treasury with a reliable stream of revenue to fund public services, it simultaneously reduces the take-home pay of citizens who are already struggling with the rising cost of essentials. This reduction in disposable income has a direct impact on consumer confidence and spending patterns, particularly in the discretionary sectors of the economy. By diminishing the financial incentives for career advancement and overtime, fiscal drag risks creating a productivity trap that could hamper the nation’s ability to generate the very growth needed to escape the current stagnation.

Compounding the effects of fiscal drag is a wider array of tax increases targeting business rates, council taxes, and investment income, which together form what some analysts describe as a “blizzard” of taxation. These cumulative measures are particularly damaging to the rental market and the small business sector, where landlords and entrepreneurs are finding it increasingly difficult to justify the risks associated with investment. The hike in taxes on dividends and rental income has already begun to drive some private landlords out of the market, leading to a shortage of available housing and further inflating rental prices for tenants. This contraction in the private rental sector adds to the general economic malaise, as labor mobility is restricted by the lack of affordable accommodation in high-growth areas. The current approach to taxation appears to prioritize short-term fiscal consolidation over the long-term health of the private sector, raising concerns about future stability.

The economic landscape of the United Kingdom reached a critical juncture where the rigidity of fiscal policy began to clash directly with the operational realities of the private sector. To navigate these challenges, the government was encouraged to adopt a more flexible approach by conducting a radical review of welfare spending and postponing the implementation of planned tax hikes to stimulate business confidence. It became clear that prioritizing investment-led growth over immediate tax revenue was necessary to stabilize the manufacturing and retail sectors. Analysts recommended that the Treasury pivot toward policies that incentivized domestic energy production and reduced the burden of fiscal drag to restore consumer purchasing power. By fostering a more resilient and adaptable economic framework, the nation could have mitigated the risks of a protracted recession and laid the groundwork for a more sustainable recovery. These strategic adjustments represented the most viable path forward in a global environment defined by volatility.