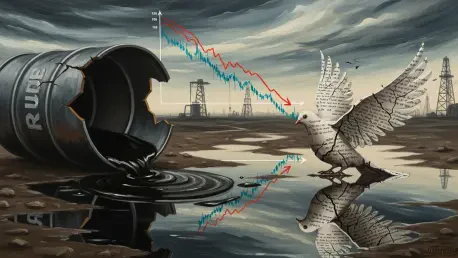

Market Instability: The Great June Price Contraction

The global energy landscape shifted with startling speed this month, as Brent crude recorded a massive twenty-one percent decline to settle at seventy-two dollars and ninety-two cents per barrel. This monthly drop represents the most significant contraction seen since the height of the global pandemic, leaving West Texas Intermediate trailing closely at sixty-nine dollars and fifty cents. While immediate relief at the fuel pump might suggest a return to normalcy, the underlying variables hint at a volatile foundation. Analysts are currently dissecting whether this price correction stems from a genuine shift in supply fundamentals or if it merely reflects a fleeting pause in geopolitical hostilities that could reignite at any moment.

Historical Context: The Impact of Military Friction

To grasp the magnitude of this downturn, one must account for the persistent supply constraints that defined the early months of this year. Before the current slump, oil prices remained artificially inflated by military friction between the United States and Iran, which generated significant distribution bottlenecks and high-risk insurance premiums. Historical patterns show that energy markets are uniquely hypersensitive to Middle Eastern conflicts, particularly when maritime security is compromised. Although current prices have receded, they remain higher on an annual basis than in previous cycles, indicating that the scarcity driven by strategic maneuvering has not vanished.

Deciphering the Drivers of Diplomatic De-escalation

Maritime Security: The Strait of Hormuz and the 14-Point Memorandum

The primary catalyst for the mid-June sell-off was the signing of a fourteen-point memorandum on June seventeenth, intended to pause active hostilities and restore traffic through the Strait of Hormuz. Because this waterway facilitates roughly twenty percent of the world’s oil transit, its reopening served as an immediate pressure release for global supply chains. This agreement successfully lowered the maritime insurance costs that had previously burdened cargo ships traveling through high-risk zones. Nevertheless, this memorandum functions as a temporary measure, lacking the comprehensive details needed to resolve long-standing territorial disputes in the region.

Diplomatic Disconnect: Contradicting Narratives in Washington and Tehran

While the memorandum provided a brief moment of market clarity, the ensuing diplomatic activities in Doha, Qatar, have introduced a thick layer of geopolitical fog. Officials from Washington claim that Tehran initiated the request for these high-level meetings following recent strategic airstrikes, yet the Iranian Foreign Ministry has issued firm denials. Tehran maintains that its presence in Qatar is entirely unrelated to any Western-led diplomatic initiatives, creating a “he-said, she-said” environment that complicates market forecasting. Such a stark disconnect between the two primary actors suggests that any perceived peace might be built on a mutual need for a tactical pause rather than a shared resolution.

Trader Sentiment: The Dangers of Premature Optimism

Financial strategists are expressing concern that the sheer velocity of the recent price drop indicates a market that is overestimating regional stability. Many traders are essentially pricing in a definitive peace treaty while ignoring the structural complexities of nuclear enrichment and regional power dynamics that originally fueled the fire. Skeptics argue that treating the current sixty-day negotiation window as a guaranteed success creates a dangerous false floor for crude prices. Historical case studies demonstrate that temporary ceasefires often precede rapid price reversals once diplomatic talks reach an inevitable stalemate.

Future Projections: The Critical 60-Day Window

The trajectory of energy costs over the next two months depends entirely on the narrow window of time established in the interim agreement. Negotiators must navigate deeply entrenched issues, such as the specifics of nuclear enrichment limits and the complex framework for lifting economic sanctions. If these discussions fail to produce a binding long-term accord within the allotted sixty days, a massive volatility snapback is highly probable. Under such a scenario, prices could surge back toward the one hundred dollar mark as the risk of renewed supply disruptions returns to the forefront of global trade.

Risk Management: Strategic Takeaways for Industry Leaders

For organizations and private investors, the current price environment requires a strategy of cautious skepticism rather than aggressive long-term commitment. Hedging against potential spikes remains a prudent move, especially as the fundamentals of the market continue to be dictated by unpredictable diplomatic signals. Industry leaders in the logistics sector should maintain active contingency plans and alternative shipping routes despite the current reopening of the Strait. Staying liquid and reactive is essential, as the current market lows are not yet supported by a change in global demand metrics.

Final Assessment: Navigating an Uncertain Energy Landscape

The collapse of oil prices in June provided a temporary reprieve for the global economy, yet the underlying instability of the Middle Eastern corridor persisted. Strategic actors recognized that the diplomatic breakthrough in Doha lacked the structural integrity required for long-term market confidence. Decision-makers implemented robust risk-management protocols to mitigate the danger of a sudden reversal in maritime security. Ultimately, the industry shifted toward decentralized supply chains and invested in alternative energy storage to reduce dependency on the Strait of Hormuz. These actions served as a buffer against the inevitable return of price volatility as the negotiation window began to close.